What is a stock portfolio?

Investing in a stock portfolio is a way of trying to profit from increases in the share price of a range of companies rather than simply betting on one.

By owning shares in a range of companies – carefully chosen to represent a balance of different sectors and company types – you have more control over the risk associated with equity investment.

The idea is that if one of the stocks you invest in falls in price, this will be more than compensated for by increases in the price of other stocks in your portfolio.

Learn while practicing

You can build a pretend portfolio with

Google finance and then discuss your pretend investments in the thread.

Putting a portfolio together

Building a stock portfolio is a highly personal process and requires some intense self-scrutiny.

How you shape your portfolio will depend on everything from your current income, your attitude to risk and your age to what you want the money for and when.

Throughout this module, we will show you how to build a "conservative growth" portfolio, but first it is important that you understand portfolios in general, and what you want to achieve by building one.

First identify your goals and time horizon

Before you start investing it is vital that you develop a strategy based on who you are and why you are investing.

Forming a clear idea of your own financial goals and how much risk you are prepared to take will vastly improve your chances of success.

So before you buy a single share, ask yourself the following:

What is my risk/reward profile?

Understanding your attitude to risk and reward is arguably the most important step when planning your investment strategy. You might be attracted to the prospect of great performance, but how much risk are you willing to take to achieve it?

How much money do I want and what do I want it for?

Be clear about why you are investing. Perhaps you want to save up a deposit to get on the housing ladder. Perhaps you want to save for retirement. Perhaps you simply want a financial safety net if ever your circumstances take a turn for the worse.

Whatever you want, work out how much money you will need and when you're likely to need it. Break down your goals into short (1-3 years), medium (3-5 years) and longer-term (5+ years) time frames. If you don't need the money for a decade, for example, you can usually be more aggressive in your investment strategy and take on more risk than if you need the money in a couple of years.

What are my financial circumstances?

Be realistic about how much money you can set aside for investment and how much money you expect to earn in the future. You may aspire to earning a six-figure salary in the next five years, but is that really going to happen? There's no point starting to invest more money than you can afford if that means you're going to dip into your stock portfolio prematurely. Conversely, if you expect to inherit a large sum of money, you can – with caution – factor that in to your calculations when you decide how big an investment pot you aim to achieve.

How old am I?

The life stage you are at will be a big factor when you decide how to invest. Generally, the younger you are, the greater level of risk you can afford to take in your investments. Markets move in cycles, pulling down stock markets and pushing them up, sometimes for several years at a time. If you are about to retire therefore, you cannot afford your last economic cycle as an investor to be a downturn. A young professional however can afford to be more long term, watching investments ride out numerous market ups and downs.

What are my personal plans?

Be clear about how a change in circumstances will change your priorities as well as your ability to achieve your goals. If you plan to have children, for example, you may want to start investing for their education. You may however find you have less money to invest as the costs of a bigger home and childcare erode your income. If you plan to divorce, you could see your costs/income rise or fall, depending on the settlement.

Risk and your portfolio type

Risk is a crucial concept in investing. It refers to the possibility of losing some or all of your original investment and varies widely depending on asset classes, share sectors, company size and market conditions.

Very volatile shares that have a high risk of falling in value usually also have a higher than average chance of rising in value. Very stable shares that represent a lower risk of falling in value also represent a smaller opportunity in terms of probable growth.

Share portfolios can be broadly categorised in terms of how much risk they expose you to as well as the nature of their potential rewards. The following will outline the common types of portfolios:

Growth portfolio

A so-called growth portfolio is right for you if you want to see the value of your investment rise fast but to achieve this you are also prepared to face the risk that it might fall in value. This kind of portfolio will include a greater proportion of higher-risk shares – for example in small-cap or cyclical companies – which also have a greater chance of experiencing big increases in value.

Income portfolio

An income portfolio conversely is one that is tailored to include very little risk. It is the right type for you if you are more interested in taking a steady income from your investment than watching it grow, but are not prepared to see it lose any of its value. It will be mostly made up of very stable companies whose shares prices may only grow very slowly but which are very unlikely to fall in value and which pay good, regular dividends.

Conservative portfolio

A conservative growth portfolio – the type that we will show you how to build in this module – is right for you if protecting the value of your investment is very important for you but you are prepared to take on a little risk to help drive moderate growth too.

The building blocks - growth, income, defensive, cyclical and speculative stocks

The different kind of portfolios outlined above achieve their targeted risk and reward by carefully tailoring the proportion of so-called 'growth' and 'value' stocks they contain as well as the mix of 'cyclical', 'defensive' and 'speculative' stocks.

Growth stocks

Growth stocks are those that are expected to see their value rise faster than the rest of the stock market, based on their historical performance. They expose you to more risk over time, but usually offer greater rewards in the end.

Income stocks

Income or 'value' stocks are those that pay better dividends than other companies in the stock market.

Defensive companies are those whose products and services remain in demand whether an economy is expanding or contracting. These include pharmaceutical companies, utility companies and many food and beverage companies. They are considered a safe, stable investment.

Cyclical companies

Cyclical companies are those that perform very well when the economy is expanding and perform badly when it is contracting. These include banks, airlines and construction companies. They are considered a risky investment but one that can drive excellent growth when the market conditions are right.

Speculative stocks

Speculative stocks are those of young companies whose future is unknown but who could surge in value if things go well – for example an energy explorer hoping to strike oil. They are considered very high risk.

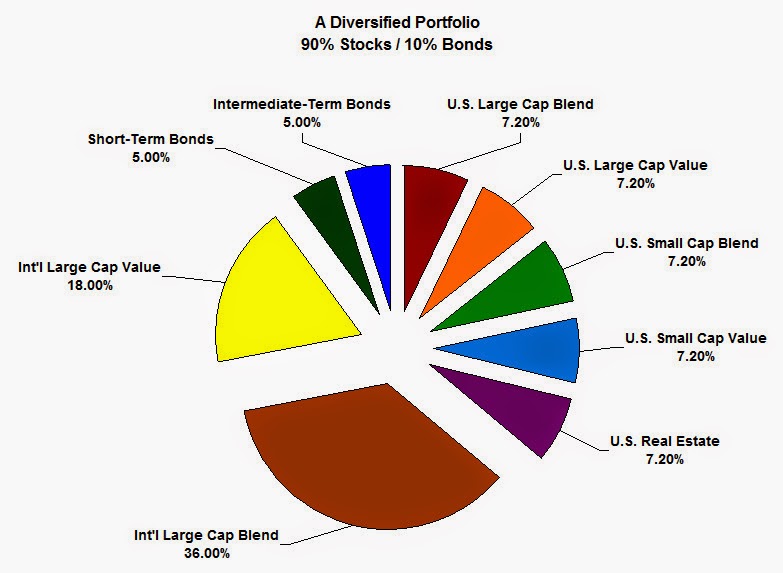

Diversification

Regardless of whether you invest in a growth, income or conservative growth portfolio, it should always include shares in a decent number of different companies – preferably at least 15.

Investing in a wide range of stocks that give you exposure to different kinds of industry sectors spreads your risk across the market and should help your portfolio grow steadily regardless of market conditions.

.jpg)

.jpg)